Volatility, competition and consolidation are the best words to sum up 2015 in terms of local firms vying for business and talent in Asia-Pacific’s crowded markets.

Click here to view the Asia Pacific 150 2016 report

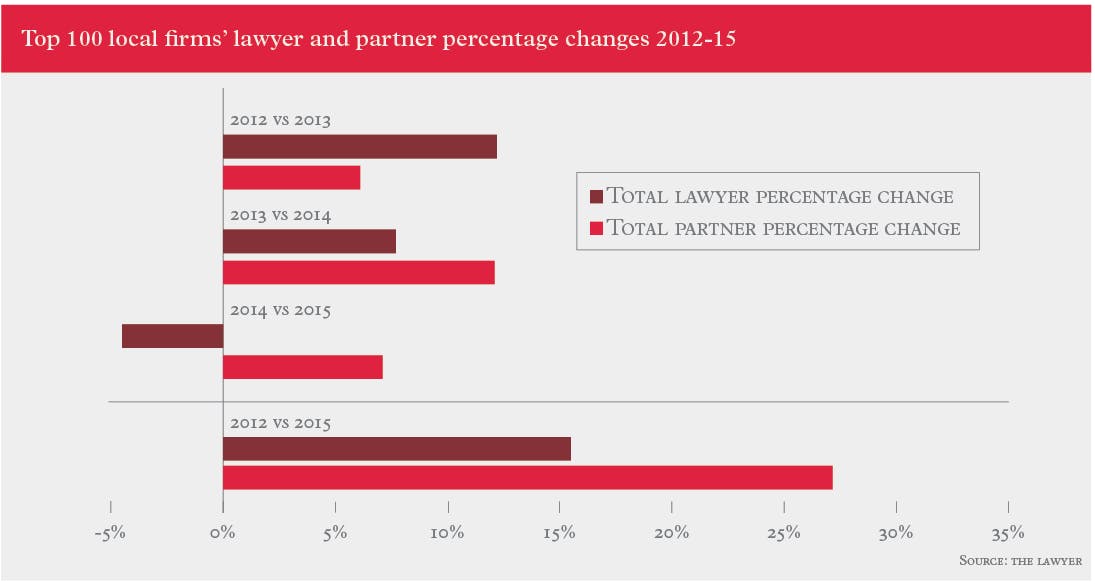

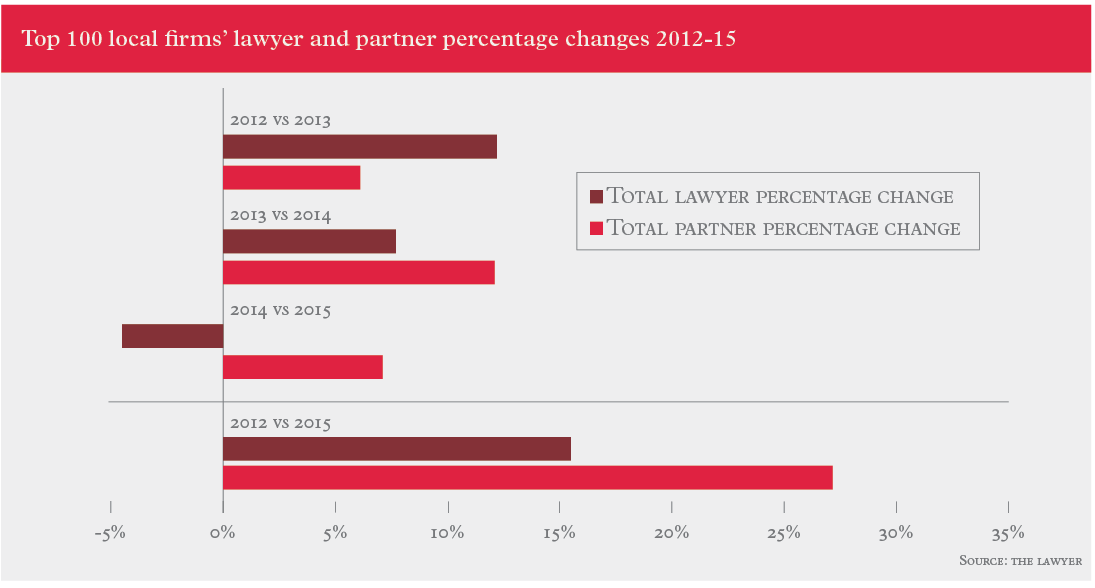

As this year’s Asia-Pacific 150 research shows, the growth rate of the Top 100 largest independent firms is slowing in comparison with recent years. Since the report’s inauguration in 2013 The Lawyer Asia-Pacific 150 has built up a dataset allowing us to benchmark firms’ development and understand and predict the pattern of the growth in the region.

This year’s largest 100 independent firms by lawyer headcount together had 38,967 lawyers in 2015. That represents a 3.1 per cent decline on the previous year’s figure, which stood at 40,208. This is the first time we have seen the headcount figure fall. However, the drop is due to Chinese giant Dacheng’s 2015 combination with global firm Dentons, which removed 3,800 lawyers from the independent Top 100 category.

This year’s largest 100 independent firms by lawyer headcount together had 38,967 lawyers in 2015. That represents a 3.1 per cent decline on the previous year’s figure, which stood at 40,208. This is the first time we have seen the headcount figure fall. However, the drop is due to Chinese giant Dacheng’s 2015 combination with global firm Dentons, which removed 3,800 lawyers from the independent Top 100 category.

On a like-for-like basis the largest 100 independents, including Dacheng, achieved a 6 per cent increase in their combined lawyer headcount. But this is still the slowest growth rate since 2012. The best year was 2013 in terms of headcount growth for the Top 100 firms, when they saw a 12.3 per cent increase over 2012. The year after the growth rate slowed to 6.9 per cent. Despite this slowdown, these firms have seen a remarkable growth pace of 16.3 per cent between 2012 and 2015.

More than half of this year’s independent firms, 59 per cent, reported an increase in lawyer headcount, while 33 saw their numbers drop. The rest were either static or new entrants.

King & Wood Mallesons, the region’s most global-facing independent firm, saw an 18.5 per cent drop in lawyer numbers, from 1,634 in 2014 to 1,331 last year.

The slowdown in headcount expansion is due to a mix of external and internal factors. It is partly affected by macro trends such as China’s economic slowdown, market volatility across Southeast Asia in 2015, and Australia’s post-mining boom blues. At the same time, there is a profound shift away from focusing on growing in size and towards upscaling and integration among some of the more established big players.

One of China’s largest firms Jun He, ranked as the 31st largest firm in the region, also reported a reduction in lawyer numbers. It has been putting an emphasis on improving its internal structure and last year overhauled its partner remuneration system to promote collaboration between partners and increase cross-selling.

“The market is not what it was five years ago, when global firms were launching in Australia with gay abandon”

Jun He managing partner Warren Hua says deepening internal organisational integration and improving service quality and efficiency are top priorities but that the size of the firm will continue to expand as the legal market in China grows.

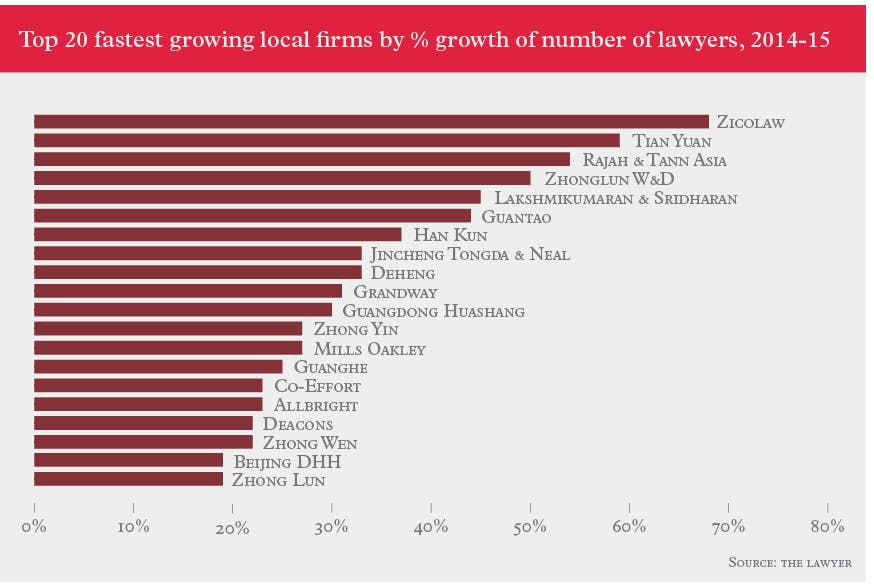

Despite its focus not being on size, Tian Yuan is the second-fastest growing firm in the Top 100 in 2015, having increased its lawyer headcount by 59 per cent, from 226 in 2014 to 360. This strong surge is a result of several team hires from rival firms, including a team of insurance partners and lawyers from AnJie.

Similar to Tian Yuan, many Chinese firms have enjoyed continued growth in the past few years and remain the most dominant group in the independent firms ranking this year. In fact, 37 of this year’s Top 100 firms are from China, two more than last year. Beijing-based Tian Tai and Han Kun are new entrants this year.

Of the 20 fastest growing firms in the region, 14 are from China. Others include Zicolaw and Rajah & Tann, both based in the ASEAN region, Indian firm Lakshmikumaran & Sridharan, Hong Kong’s Deacons and Australasia’s Chapman Tripp and Mills Oakley.

Chinese firms’ financial strength

In an encouraging sign of maturity, transparency and sophistication in the way they are managed, almost all the Chinese firms that submitted data for this year’s Asia-Pacific 150 research provided a revenue figure for 2015. Some even provided profit per partner data.

Although some of the largest Chinese firms saw a slight reduction in lawyer numbers they still achieved revenue growth in 2015. Global Law Offices’ headcount, for example, dropped by 15 lawyers to 230 last year. However, its revenue for 2015 increased by 10.7 per cent, from RMB280m to RMB310m (£30.6m-£33.9m). This is a result of the firm’s strategic push for growth in profitability, winning mandates in sophisticated transactions where fee rates are generally higher.

Similarly, Chengdu-headquartered Tahota had static headcount numbers but its revenue soared by 34 per cent, from RMB202.5m to RMB280m in 2015. The firm’s focus on development in key domestic markets such as Beijing and Shanghai as well as handling cross-border matters contributed to this strong financial performance. It opened four offices last year, in Jinan, Kunming, Shanghai and Washington DC – its first base in the US. Jun He also raked in RMB1.17bn in 2015, 17 per cent higher than its 2014 revenue of RMB1bn. This signifies a dramatic jump of 66.7 per cent in revenue per lawyer, from RMB1.86m to RMB3.1m.

The fastest growing firm by percentage revenue is Chongqing-based Zhonghao. In 2015 it had 201 lawyers but turned over RMB250m, more than doubling its revenue of RMB120m the previous year.

The top 10 fastest growing firms’ average speed of revenue increase was a staggering 62 per cent. Strong financial results are not exclusive to the emerging and regional firms. The country’s largest top-tier firms have also reported stellar results. Zhong Lun and AllBright, two of the countries highest earning firms, increased their 2015 revenue by 34 per cent and 48 per cent respectively. Zhong Lun is now China’s top independent firm by revenue, with nearly RMB2bn in 2015.

Shrinking markets

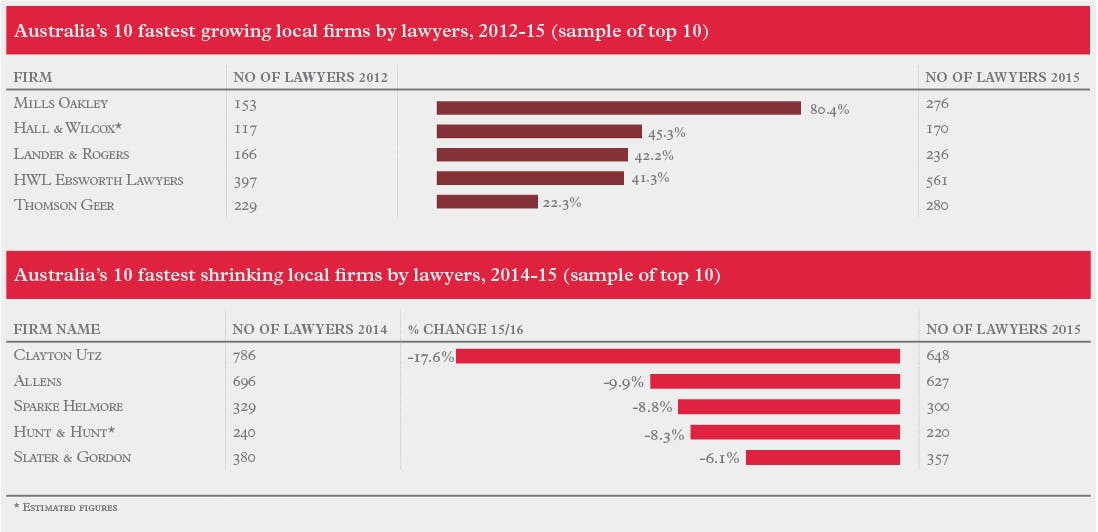

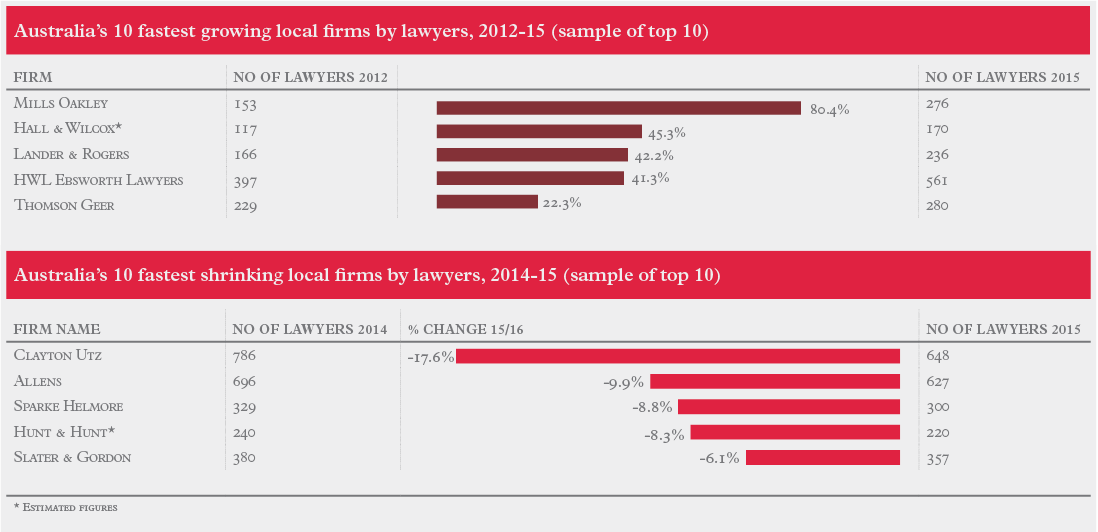

The only jurisdiction that has seen a significant number of shrinking firms is Australia. It was a year of mixed fortunes for firms in this mature and highly competitive market.

Nine of the 22 Australian firms in this year’s Top 100 shed numbers. Two Australian firms, DibbsBarker and HopgoodGanim, dropped out of the table. DibbsBarker’s headcount fell by a whopping 25 per cent after the Canberra office split from the firm.

The biggest fall in qualified lawyer headcount was at Clayton Utz, which saw a 17.6 per cent decrease to 648, with partner numbers falling by 10 partners to 174. But despite the reduction in headcount the firm reported revenue growth of 2.4 per cent , with total turnover reaching $428.4m in 2014/15.

Linklaters’ alliance firm Allens witnessed a similar fall in headcount, with average qualified lawyers dropping by 16.7 per cent to an estimated 580 in 2015. This figure is considerably smaller than the 815 qualified lawyers and 203 partners it reported in our first Asia-Pacific report in 2013.

In the past five years the amount of work available to firms has undoubtedly decreased. According to a report by Thomson Reuters, demand for commercial legal services has been on a steady decline for five years and 2015 failed to arrest this trend, with demand again falling by 2 per cent.

This is primarily attributable to a drop in demand for the industry’s three biggest practice groups: dispute resolution, banking and finance, and general corporate work, which represent 48 per cent of all legal services provided.

Meanwhile the weakening Australian dollar, the dire state of the mining sector, increased in-house capability and rapidly progressing disruptive technology have been big challenges for firms. There is no doubt that the market is not what it was five years ago when global firms were launching in Australia with gay abandon.

As a result, there has been notable cutting of headcount at a number of the larger firms, as they bid to remain profitable. Headcount at Australia’s five largest independent firms was 3,096 lawyers in 2015, compared with 3,263 the previous year, a fall of 5.2 per cent.

Nevertheless, a number of mid-tier firms have fared better and continued to grow. HWL Ebsworth has made its presence felt in the past couple of years. In 2015 it muscled its way into fourth spot on our headcount table. It now boasts 56 qualified lawyers, up 9 per cent on 2014 and a whopping increase of 42.1 per cent on the 397 lawyers in had in 2012. The other rapidly growing national firm is Mills Oakley, which has grown headcount by more than a quarter, to 276 qualified lawyers and 76 partners.

Japan is another market where firms’ growth is stalling. The total number of lawyers in the top five firms stood at 1,923, marking a 7.3 per cent decrease from the total of 2,074 in 2014. Among the five firms, three achieved modest increases, with Anderson Mori & Tomotsune growing at the fastest rate of 3.4 per cent. Its growth is mainly due to the bolt-on of a 50-lawyer team from the Tokyo office of now-defunct Bingham McCutchen in April 2015.

Outward visions

Another sign of Asian firms becoming more mature is their growing appetite for expansion beyond national borders and servicing major domestic clients in global matters. A high proportion of this year’s Top 100 firms have opened new offices. A particularly well-travelled path is North Asian firms – those based in China, Japan and South Korea – heading South. Some have launched a base in Hong Kong while others are jostling for position in Southeast Asia.

Most notably, South Korean firms are rushing to open in Vietnam and other Southeast Asian countries. In 2015 the country’s second largest firm by revenue, Bae Kim & Lee (BKL), opened two offices in Vietnam.

Yulchon, fourth largest by revenue, opened in Vietnam back in 2007 and in Myanmar in 2014. Last year, it ventured further afield by opening an office in Moscow. Jipyong, ranked 98th in this year’s Top 100, has already established an extensive platform across South Korea, with six local offices. Last year it also opened an office in Moscow and then in Iran through a partnership with local firm Gheidi & Associates.

Kim & Chang, South Korea’s largest firm by both lawyer number and revenue, decided to stay out of the increasingly crowded Southeast Asia market and opened an office in Hong Kong.

“As South Korea’s legal market enters the third phase of liberalisation it is critical that foreign and domestic law firms alike enhance their overseas service offerings to Korean companies,” predicts BKL corporate partner Sky Yang. “While the general economic outlook in Korea leaves much to be desired, we expect domestic companies’ overseas investments will continue to rise.”

Japanese firms, which made inroads into Southeast Asia in a big way in 2013 and 2014, have continued to expand, albeit at a slower pace. Last year both Anderson Mori & Tomotsune and Mori Hamada & Matsumoto opened Bangkok offices. Their domestic rivals Nishimura & Asahi and Nagashima Ohno & Tsunematsu had already entered the Thailand market, in 2013 and 2014 respectively.

Chinese firms are also expanding globally, but mostly with a focus on Hong Kong and Western markets. Last year Jingtian & Gongcheng became the latest mainland firm to set up an office in Hong Kong, forming an association with Mayer Brown JSM. AllBright, Han Kun and Llink Law Offices are among those that opened an office in the same year.

Outside Asia, Chinese firms have been expanding into the US. Zhong Lun is leading the pack by launching two offices, in Los Angeles and San Francisco, following a team hire from the US offices of legacy Dacheng, which has merged with Dentons. It already has an office in New York, established in 2013. Tahota is another firm that has ventured into the US with a Washington DC office and it is planning to tap into New York in the near future. Its Western region-based rival Zhonghao also planted a flag in the US – in New York – earlier this year.

AllBright, the fifth largest independent firm in Asia-Pacific with 1,229 lawyers, is also contemplating a move outside Asia. But instead of New York, it has set its eyes on the financial centre of Europe. It plans to open an office in London.

Zhong Lun is the only top Chinese firm to have a branch office in London, although its two large Chinese rivals, Yingke and Zhong Lun W&D, extend their services to the UK through strategic alliances. Yingke entered into an alliance with UK 200 firm Memery Crystal in 2015 and Zhong Lun W&D has been in a relationship with London boutique DKLM since 2012.

To purchase the full report contact Richard Edwards on +44 (0) 207 970 4672 or email richard.edwards@centaurmedia.com

International firms in Asia-Pac

Growth for the Top 50 international firms in the Asia-Pacific was at a much more measured pace in 2015, and those with a focused service approach achieved the best results.

Markets in the region have been volatile since 2015 as a result of plunging global oil prices, slowing growth in China, political uncertainty in Southeast Asia and Australia’s mining boom grinding to a halt. The result is that international firms in the region, with their vastly different sizes, development stages, strategies and practice and sector focuses, showed mixed performances last year. However, as a group their combined lawyer headcount increased modestly during 2015, up 3.6 per cent from 10,134 in 2014 to 10,494.

We have taken out Dentons’ figure for a like-for-like comparison. The global firm’s ground-breaking deal with Chinese giant Dacheng in November 2015 has bumped up its Asia-Pacific headcount by 7,635 per cent, from 50 in 2014 to 3,945 at the end of last year. If Dentons’ figure were included, the Top 50’s growth rate would be distorted to a much higher pace of 42 per cent.

Growth seekers

Looking at individual firms’ performances, the fastest expanding international advisers are the legal services units of the Big Four accountancy firms. The average speed of headcount increase among KPMG Legal, Deloitte Legal, EY Law and PwC Legal was 44.6 per cent in 2015.

KPMG Legal has emerged as the fastest growing firm in Asia-Pacific, as its number of lawyers jumped 134.4 per cent from 32 to 75. Last year, it was ranked 50th in the Top 50 table but its ranking moved up swiftly to 40th in this year’s report.

KPMG Legal has emerged as the fastest growing firm in Asia-Pacific, as its number of lawyers jumped 134.4 per cent from 32 to 75. Last year, it was ranked 50th in the Top 50 table but its ranking moved up swiftly to 40th in this year’s report.

Deloitte Legal came in fifth in terms of headcount increase, with a 27.1 per cent increase, from 140 to 178, overtaking its law firm rivals such as Clyde & Co, Morrison & Foerster (MoFo) and Sidley Austin to become the 17th largest (for a detailed analysis on the Big Four accountancy firms, read the full Asia-Pacific 150 report).

Among the traditional legal services providers, UK firm Stephenson Harwood’s lawyer headcount rose sharply by 32.6 per cent from 86 to 114. Much of the increase is down to the firm’s efforts in building up several new offices that it has launched over the past two years, such as the Beijing office, the Seoul office and an alliance in Singapore.

Eversheds and Kennedys have also seen similar rates of headcount rises.

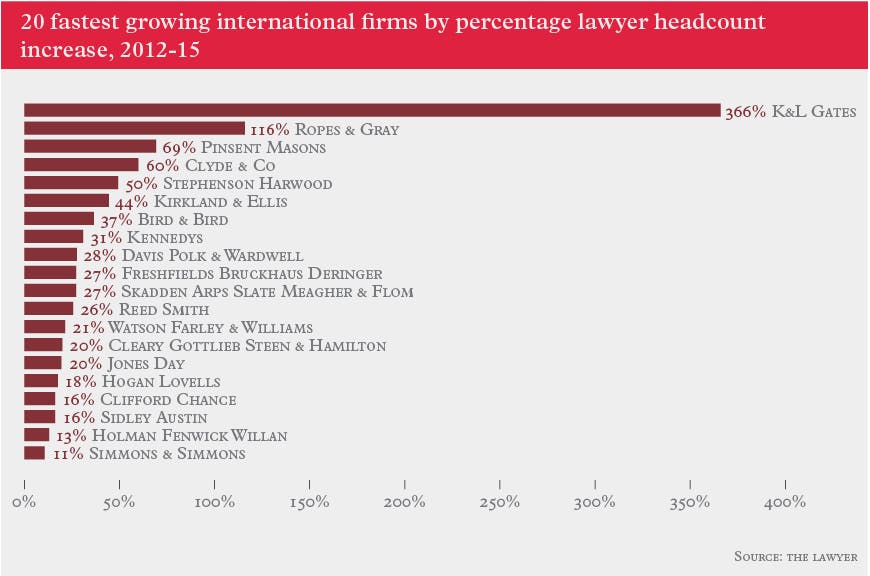

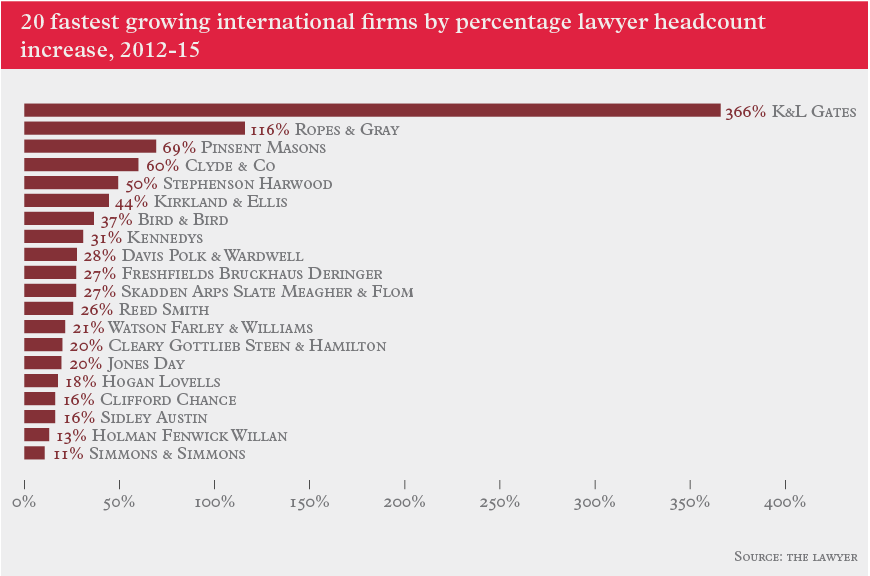

Ropes & Gray is the fastest growing US firms in the region. It added 19 lawyers in 2015, resulting a 25 per cent surge in lawyer headcount. Its partner number also increased by four from 21 to 25. DLA Piper, Reed Smith, Squire Patton Boggs and Sullivan & Cromwell are among the other US firms to have bulked up in Asia-Pacific last year.

According to The Lawyer’s research, 46 per cent of the Top 50 firms reported an increase in lawyer headcount in 2015, while 44 per cent of the firms saw a reduction or stayed static.

The firm that has seen the largest shrinkage was Freshfields Bruckhaus Deringer, where lawyer headcount dropped by 16 per cent from 250 in 2014 to 210 in 2015. However, the firm added two partners in 2015, pushing its total number of partners in Asia to 35.

UK firm Bird & Bird and US firms K&L Gates, MoFo and O’Melveny & Myers are also on the fastest shrinking firms table this year.

Taking a four-year view, O’Melveny had endured the steepest drop – 45.5 per cent between 2012 and 2015. It was followed by Paul Hastings and White & Case, which are the second and third fastest shrinking international firms according to our research.

Slimming down on the top

A notable trend in Asia-Pacific last year is that some of the largest firms had been trimming numbers. Five of the Top 10 largest firms had cut their lawyer headcounts. For example, the region’s second largest global firm, Baker & McKenzie, reported a 3.6 per cent dip, reducing its lawyer number from 1,227 to 1,183.

Herbert Smith Freehills (HSF), which came third in this year’s ranking, had a 4.6 per cent reduction in lawyers, from 960 to 916. The 2015 headcount represents an even bigger plunge (-18.5%) when compared to its 1,130-lawyer force in 2012, the year the firm’s Australia merger went live. Similarly Ashurst and Norton Rose Fulbright also had considerable shrinkage in lawyer numbers over the four-year period.

In the case of Ashurst, HSF and Norton Rose Fulbright, their Asia-Pacific operations were bolstered significantly following their respective mergers with Australian firms several years ago. The gradual decline in headcount over the past year is partially due to the slowdown in Australia (see Australia market analysis on page 42) and post-merger integration between their large bases in Australia and offices in Asia.

In Australia, both Ashurst and Norton Rose Fulbright are understood to have shrunk their partnerships substantially. In the four years that The Lawyer has been running its Asia-Pacific 150 survey, Ashurst’s partner numbers have fallen 18 per cent to 147 in 2015, with the partnership shrinking by 12 per cent in the past 12 months alone. Meanwhile, Norton Rose Fulbright’s partnership numbers fell from 140 in 2012 to an estimated 132 last year.

The challenging market conditions also led to Skadden Arps Slate Meagher & Flom’s office closure in Sydney, the first global firm to exit the country since the departure of Dorsey & Whitney in 2013.

However, the struggle of some global giants hasn’t totally stemmed the flow of new entrants into the market. In its bid for global domination, Dentons announced in November its intention to merge with 434-lawyer Australian firm Gadens, increasing the former’s already massive size in Asia-Pacific.

Top-line challenge

In this year’s Asia-Pacific 150 questionnaire, we asked firms to provide their Asia-Pacific revenue for 2015 but only a dozen of firms disclosed their figures. Thanks to these firm’s financial data, the research is able to take a rare glimpse of the most sensitive issue among international firms doing business in the region – how much money are firms making in the highly competitive region?

The results are not so encouraging and proves the common perception that stepping up revenue in Asia’s competitive and volatile markets is challenging.

Among the firms that provided a regional turnover figure, Baker & McKenzie is the highest gross earning firm. In its 2015 financial year ending 30 June, its 17 offices in Asia-Pacific turned over $607m, equating to 25 per cent of the firm’s global revenue of $2.43bn.

But its revenue in Asia-Pacific has been on a downward turn over the past two years. Its financial year 2015 Asia-Pacific result was down by 8.3 per cent from $662m in the previous financial year, which in turn was a 2.2 per cent dip from $677m in 2013. The firm blames the strength in the US dollar, the firm’s reporting currency, as the main reason behind the decrease in its regional and global revenues last year.

A spokesperson says the firm’s forecast revenues for the 2016 financial year show strong double-digit growth in US dollar terms – even though the foreign exchange headwinds continue.

By revenue, DLA Piper is the second largest international firm in the region, raking in $315.5m in 2015 from the region. It marks a 16 per cent increase on its 2014 revenue of $271.9m. But a large part of that growth is the result of a non-financial merger in New Zealand in 2015. Viewed on a like-for-like basis, the firm’s regional revenue increased 2.8 per cent to $279.6m (without New Zealand), accounting for about 11 per cent of the firm’s global revenue of $2.5bn.

Clifford Chance, the largest magic circle firm in the region, comes third with $303.4m (£205m). Although its Asia-Pacific headcount was static, its Asia-Pacific revenue for the financial year 2014/15, ending 30 April 2015, saw a five per cent increase from $289.06m in 2013/14 to $303.88m. Modest regional growth came against a trying year globally, as the firm reported a 0.7 per cent dip in global turnover from $2.03bn to $2.02bn. The region contributed 15.2 per cent of the global total. Over a four-year period, the firm achieved a 10.8 per cent increase in revenue, from $274.38m in 2011/12 to $303.88m.

“We have a very focused business plan which leads to the ability to invest significantly in a limited number of areas”

Hogan Lovells and K&L Gates come in closely at fourth and fifth position after Clifford Chance, with $127.4m and $120.7m respectively. While Hogan Lovells achieved a 2.3 per cent increase from $124.5m in the previous year, K&L Gates’ figure was down by 14.8 per cent from the $141.7m recorded in 2014 and 18.3 per cent lower compared to the 2013 figure of $147.8m.

K&L Gates Asia managing partner David Tang says a plummeting Australian dollar exchange rate makes it difficult to provide a fair like-for-like comparison, but the Asia practice had been the primary beneficiary of K&L Gates’ growing global platform. He adds that the Asia offices’ contribution to the global platform is larger than the dollar value due to the increasing number of outward referrals from Asia offices.

For most of these firms, Asia-Pacific’s contribution to their global revenues is still relatively small, mostly under 10 per cent. Although none of the managing partners at the firms would give a target to which they would like to grow the percentage, all have confirmed that Asia-Pacific remains an important region for their firms and that they will continue to invest there.

RPL gaps

Among the firms that provided regional turnover information, Clifford Chance has the highest revenue per lawyer (RPL) figure in 2015, at $697,000 per lawyer. It is 15 per cent lower than the global average of $802,000.

Hogan Lovells has the second highest RPL in the region, $531,000, which is short by 21.6 per cent from its global average of $678,000 per lawyer.

All firms’ Asia-Pacific RPL figures are lower than their firm-wide global average.

However, the gaps are much narrower when comparing regional and global revenue per partner (RPP) figures.

Focused growth

Some of the firms that achieved strong growth organically last year share a similar strategy. DLA Piper, Reed Smith and Ropes & Gray, for instance, have adopted a focused approach to their Asia-Pacific strategy, investing in their core sectors and areas where they have competitive strength globally.

In 2014, DLA Piper overhauled its Asia management structuring, scrapping the managing partner role and introducing a three-member Asia committee chaired by US partner Terry O’Malley. It was followed by a period of restructuring and reshaping its practices in the region, resulting in a notable number of partner departures.

In 2014, DLA Piper overhauled its Asia management structuring, scrapping the managing partner role and introducing a three-member Asia committee chaired by US partner Terry O’Malley. It was followed by a period of restructuring and reshaping its practices in the region, resulting in a notable number of partner departures.

But in 2015, the firm started to reap the benefits of the regional shake-up. O’Malley confirms that revenue of the Asia offices (excluding Australia and New Zealand) increased 13 per cent year-on-year in 2015 and profitability was also up and stood above the firm’s global average in the most recent financial year.

“Much of what I was involved in was restructuring our practice in Asia to better align it with our global business, in terms of what kind of clients we’re serving and what kind of work we’re doing for them,” he says.

“Having that under way, we’ve started to add selected partners to build out quality in the key areas we want to focus on. We’ve been busy on that front,” he adds.

According to the Asia committee, the firm’s improving performance in Asia is a result of two simple things: strong discipline and a refined focus.

Reed Smith is this year’s fifth fastest growing international firm, and takes a similar view on Asia. It increased its regional lawyer headcount by 21.2 per cent from 113 to 137.

The firm’s managing partner for Europe, Middle East and Asia Roger Parker regards this as organic and incremental growth with a strong focus on the firm’s global sector strategy.

“Our goal is to grow revenues step by step and push up profitability. We expect to see gradual growth, and are not looking for stunning growth,” says Parker.

Ropes & Gray Asia managing partner Arthur Mok also attributes his firm’s growth amid the tough market conditions to its “narrow focus”.

“We’re not trying to be all things to all people. We have a very focused business plan which leads to the ability to invest significantly in a limited number of areas,” Mok says.

“In Asia, many firms have difficulty in selecting the markets and industries they want to serve. But our firm doesn’t take on a broad array of businesses. We only focus on core global competency in three sectors: life sciences, private equity and the newly added real estate sector,” he continues.

“The old way of trying to be everything to everyone is a hard model to pursue today. It’s difficult to compete with fast maturing local firms that have different cost structures and billing rates. It’s hard to be successful and to attract talent when operating under a tough business model and hard to make investment when there are so many different areas to cover,” he says.

Ropes & Gray’s steady progress in the past nine years is testimony to its focused strategy. It opened its first Asia office in Tokyo in 2007 and has grown to a sizable regional operation with over 100 fee-earners across four offices.

“Our mission is to continue understanding where we add value and compete in a differentiated way. We generally look to specialised areas and cross-border matters that require global industry experience. That’s where the role for international firms will be in the next 10 years,” Mok says.

Alliances and acquisitions

The Asia-Pacific region has proved a fertile ground for law firm combinations in the past five years, whether it be international firms seeking to enter the region or expand an existing presence, or local players looking to add heft in the face of ever-increasing competition.

The four-year data collected by The Lawyer’s Asia-Pacific 150 research shows that many of the region’s largest firms and fastest growing firms have achieved that status by such action.

Greater China and the ASEAN regions are two places where merger activity has been strong in the past few years, either between local firms or cross-border tie-ups.

Fastest growers

Chinese firms AllBright, Grandall and Guantao and ASEAN-based Rajah & Tann and ZicoLaw, are among the fastest growing firms over the four-year period since The Lawyer launched its first Asia-Pacific 150 report in 2013. They have all expanded in their home region by merging with or acquiring smaller local firms.

Between 2012 and 2015, AllBright and Grandall increased their lawyer headcount by 70 per cent and 51 per cent respectively due to national expansion via absorbing existing firms in second-tier cities across China. Their smaller competitors Tian Yuan and Ashurst’s Chinese ally Guantao

have grown at an even faster rate, both almost doubling their headcounts during the four-year period as they have added multiple new offices and teams.

Shanghai-based Boss & Young is the fastest growing firm in the region over the four-year period. In 2012, it was a 20-lawyer boutique but via a 2014 merger with Shanghai rival Zhongjian. The merged firm now has over 160 lawyers.

This year’s new Top 100 entrant, Tian Tai, is also the result of a merger between two Beijing-based mid-sized firms Juntai and Tianchi Hongfan. Shandong-based Jointide has also bumped up its ranking as a result of a tie-up between Zhongcheng Renhe and Qingtai.

Singapore, which is at the centre of the Association of Southeast Asian Nations (ASEAN) market, has seen the most activity outside of China.

Eight local firms now have offices in three or more ASEAN countries, the largest by headcount being Singapore’s Rajah & Tann, Allen & Gledhill and Wong Partnership. When their alliances and associations are taken into account the firms have 569, 426 and 352 lawyers working across the ASEAN respectively and 201, 169 and 111 partners.

In the past four years Rajah & Tann was the fastest-growing of the ASEAN firms, with its lawyer headcount increasing by 78 per cent over the period from 339 to 522, although much of the increase can be put down to the fact that the firm formed the Rajah & Tann Asia network in 2014.

Zicolaw, whose network of 15 offices is led by Malaysia’s Zaid Ibrahim & Co, began its regional expansion with a Singapore launch in 2003, with the firm adding own-branded offices and associated firms in the intervening period. Most recently it added eight-lawyer Singaporean firm Insights Law to its network.

Global tie-ups

As the centre of global economic gravity continues shifting towards Asia, global firms have responded by courting with established leading domestic firms and obtaining local law capabilities in key markets.

The trend began back in 2009 when legacy Norton Rose tied up with Australia’s Deacons. Numerous copycat deals followed, such as Herbert Smith’s 2012 merger with Australia’s Freehills and Ashurst’s combination and subsequent merger with Blake Dawson.

The focus has shifted to China and Singapore in more recent times. Global expansionist Dentons took the Chinese market by storm in 2015 when it merged with People’s Republic of China (PRC) independent giant Dacheng. The firm achieved a similar feat in Singapore in early 2016, albeit on a smaller scale, when it merged with local independent Rodyk & Davidson. Its Asia-Pacific footprint will soon be expanded significantly again after its recently announced deal with Australian firm Gadens.

Few global firms share the same growth strategy and method as Dentons. Most of the established global firms in the region have chosen to expand their local capability in a more measured and smaller-scale way.

Baker & McKenzie broke new ground by becoming the first firm to enter into a joint operation in the Shanghai Free Trade Zone (SFTZ) in April 2015, allowing it to offer PRC advice via its partner FenXun Partners.

UK firm Holman Fenwick Willan (HFW) followed suit by entering into a formal association with Shanghai-based shipping firm Wintell & Co in April 2016 under the SFTZ scheme.

Hogan Lovells’ regional managing partner Patrick Sherrington also confirms that the firm is looking seriously at forming a joint operation with a Chinese firm in the SFTZ.

Even some of the magic circle firms that have been active in the market for a long time are also exploring similar opportunities.

It is understood that last year magic circle firm Clifford Chance held exploratory talks with top-tier Chinese firms including Zhong Lun, although that particular combination came to nothing after partners at the PRC firm voted to remain independent.

Similarly, Linklaters had been on a two-year search for a suitable Chinese merger partner, but eventually chose to spin off the PRC-qualified lawyers in its own Shanghai office and forge a best-friends arrangement with them instead.

Stephenson Harwood took a similar approach, closing its Guangzhou office in September 2014 only to form a strategic alliance with the firm launched by that office’s shipping lawyer Xianming Lu three months later.

Singapore, which has a slightly more flexible regulatory regime for foreign firms, has seen an equal flurry of combinations between local and global outlets. Apart from Dentons and Rodyk & Davidson, the deal that caught everyone’s eyes last year is the merger between America’s Morgan Lewis & Bockius and local firm Stamford Law. Withers’ formal law alliance (FLA) with KhattarWong is another remarkable tie-up in 2015.

Other international firms that have added integrated local law practices in the past year include Kennedys’ joint law venture (JLV) with Singapore’s Legal Solutions and Herbert Smith Freehills’ FLA with Prolegis, RPC’s JLV with Premier Law.

UK firm Simmons & Simmons and US firm Reed Smith are are applying for an FLA. Meanwhile, Eversheds is discussing a merger with Harry Elias.

With Malaysia liberalising its legal services markets to attract foreign firms, Trowers & Hamlins gained the first Qualified Foreign Law Firm licence in Malaysia last year. More recently US rival DAC Beachcroft has applied for a licence to form a joint venture (JV) with Malaysia’s Gan Partnership and will focus on insurance and reinsurance matters in the country.

Forming alliances

The strategic alliance is another popular model that international firms are using to tap into emerging markets where merging with local firms is not economically viable or prohibited. Both local and international firms also deem it as a more flexible arrangement and a prelude to a closer relationship in the future.

It is a proven structure for firms’ expansion in the ASEAN region. White & Case and Hogan Lovells have recently sealed Indonesia alliances, with Witara Cakra Advocates and Dewi Negara Fachri & Partners respectively.

At the end of last year, Norton Rose Fulbright also entered into an association in Indonesia with TNB & Partners, a firm set up by three newly joined partners. The majority of the team in TNB are from its previous Indonesian ally Susandarini & Partners.

Taylor Wessing is a relatively new name in the ASEAN market. It gained a presence by admitting Singaporean firm RHTLaw to its international group in 2012. It has built up an extensive alliance network across the region during the past three years after the launch of its ambitious ASEAN Plus group. The network consists of eight members, including six ASEAN firms, one Korean firm and one Taiwanese firm.

“Singapore, which has a slightly more flexible regulatory regime for foreign firms, has seen a flurry of combinations between local and global outlets”

In North Asia, the number of strategic alliances have also multiplied in the past a few years. For firms wanting to build out their global reach while retaining independence, forming a close relationship with foreign counterparts is a good alternative to a merger and a membership in a loosely managed network.

In China, Han Kun signed a formal alliance agreement with Italian firm Gianni Origoni Grippo Cappelli & Partners last April. Beijing-based insurance boutique firm AnJie also formalised a long-term relationship with Kennedys at the beginning of 2015 in the form of a co-operation agreement.

One of the so-called red circle firms Jingtian & Gongcheng also took the plunge by entering into an association with Mayer Brown JSM in Hong Kong last August.

China’s largest firm by headcount Yingke set its sights on the UK market by signing an exclusive cooperation agreement with London-based Memery Crystal a few months later.

Many of the Chinese firms responding to this year’s Asia-Pacific 150 said they had been approached regarding a potential merger, some of them by several different firms. For the first-tier firms, a common consensus is that they see no urgency and real reason for a global merger. However, they need to build up their global reach and capability to service Chinese clients in their projects and investment overseas.

Tian Yuan’s managing partner Zhu Xiaohui, for example, puts forming alliance with international law firms on the top of his management agenda.

To purchase the full report contact Richard Edwards on +44 (0) 207 970 4672 or email richard.edwards@centaurmedia.com

Sample market analysis: Australia

If there was one overriding trend in the Australian legal market in 2015, it was change. Over the last 12 months, some global firms arrived while others departed; some national firms launched new offices while others shut their doors; there were firms whose headcount shrank by a quarter while others expanded by the same amount. And, in a seeming game of legal musical chairs, lateral hires were announced almost daily. It was a year of mixed fortunes for firms in this mature and highly competitive market. Additionally, over the last five years the amount of work available to firms has undoubtedly decreased.

The overall decline is mainly attributable to the fall in demand for the industry’s three biggest practice groups: dispute resolution, banking and finance and general corporate work, which represent 48 per cent of all legal services provided.

Meanwhile, the weakening Australian dollar, the dire state of the country’s mining sector, increased in-house capability and rapidly progressing and disruptive technology have set big challenges for law firms. The market is not what it was five years ago, when most global firms were launching in the region with gay abandon.

Varied performance

Noticeable cuts in headcount have been made among large firms in a bid to remain profitable. Headcount at Australia’s five biggest independent firms was 3,093 lawyers in 2015 compared with 3,263 the previous year: a fall of 5.4 per cent.

The biggest fall in qualified lawyer headcount was at Clayton Utz, which saw a 17.7 per cent decrease to 647 while its partner numbers fell by 10 to 174. But despite the drop in headcount, the firm reported revenue growth of 2.4 per cent, with total turnover reaching $428.4m in 2014/15 following a fall of 4 per cent in 2013/14.

“Fee-earner numbers have decreased in a controlled way, consistent with our projections of what clients want, where the market is and where we expect it to move,” says deputy chief executive partner Bruce Cooper. “Our revenue growth reflects that and shows we are getting it right.”

“Fee-earner numbers have decreased in a controlled way, consistent with our projections of what clients want”

Linklaters’ alliance firm, Allens, saw a similar fall in headcount, with average qualified lawyer numbers dropping 16.7 per cent to an estimated 580 in 2015. This figure is considerably smaller than the 815 qualified lawyers and 203 partners that the firm reported in The Lawyer’s first Asia-Pacific report in 2013.

Minter Ellison was the only one of the big firms to report an increase in headcount, up 3.8 per cent to 1,126 (these figures also include the firm’s associated but financially independent offices). In its integrated partnership, Minter Ellison maintains five Australian offices: four in Asia-Pacific and one in London. This part of the business announced 110 senior hires and promotions in 2015 – 60 per cent more than in the previous year. This reflected increasing capacity in high-growth areas such as commercial disputes and real estate.

The firm’s integrated offices also reported an increase in revenue for the 2014/15 financial year, growing by 2.4 per cent from A$418m to A$428m.

Global players

Several big global giants also had woes: both Ashurst and Norton Rose Fulbright are understood to have shrunk their partnership in the region, and in the four years The Lawyer has been running its Asia-Pacific survey, Ashurst’s partner numbers have fallen by 18 per cent to 147 in 2015, with the partnership shrinking by 12 in the last 12 months. Meanwhile, NRF saw its partnership numbers fall from 140 in 2012 to an estimated 132 last year.

Skadden Arps Slate Meagher & Flom decided to close its two-partner Sydney office altogether, making it the first global firm to exit Australia since the departure of Dorsey & Whitney in 2013.

That said, the struggle of such firms has not totally stemmed the flow of new entrants into the market. Dentons announced in November its intention to merge with 434-lawyer Australian firm Gadens, increasing the former’s already massive size in Asia-Pacific.

Meanwhile, UK firm Pinsent Masons opened in the region by launching a Sydney and Melbourne office.

Sample market analysis: Hong Kong

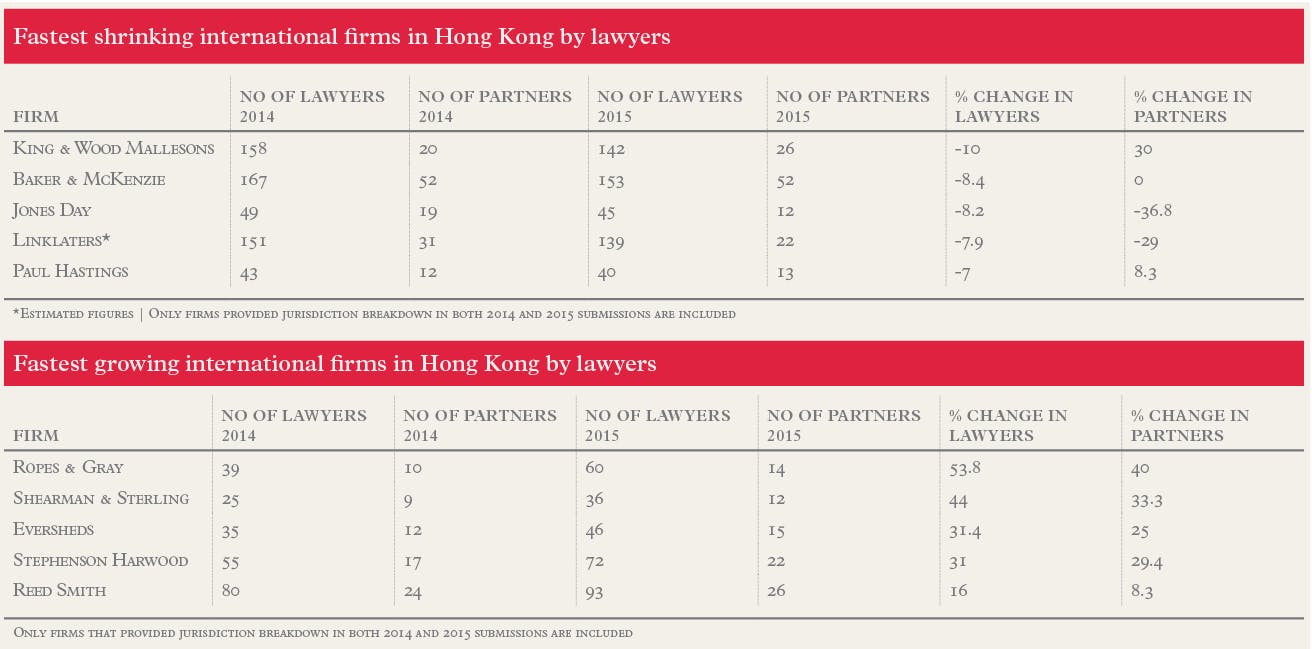

Many of the big firms in Hong Kong experienced a rather challenging year in 2015 as the city’s professional services industry was hit by China’s slowing economic growth and volatility across the wider Asia-Pacific region. The general consensus among international lawyers is that big-ticket transactions are harder to come by, competition over them is more fierce, and firms are under mounting pressure from clients to lower rates while their overheads keep on creeping up.

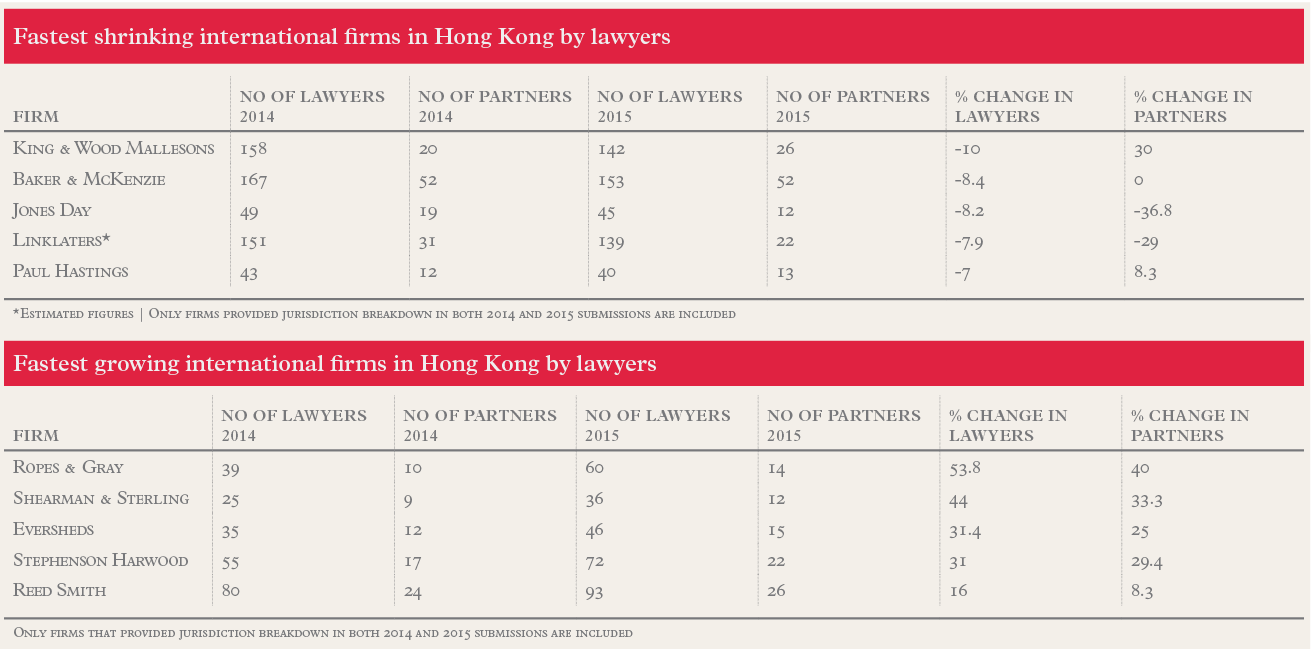

Among the larger international firms in Hong Kong a considerable proportion have seen their lawyer numbers fall. Four of the five largest international firms, for example, have seen a decrease in lawyer headcount.

King & Wood Mallesons has seen the steepest drop, down by 10 per cent from 158 in 2014 to 142 in 2015. The decrease is partly a result of continuing integration between the three legacy Hong Kong offices of the merged firm. However, the Asia-Pacific giant added six partners to its headquarters in 2015, driving up the Hong Kong partnership by 30 per cent, from 20 to 26.

Baker & McKenzie and Linklaters follow closely, with declines of 8.4 per cent and 7.9 per cent respectively in lawyer numbers. The largest international firm in town, Mayer Brown JSM, also reported a slight decrease of 3.5 per cent, from 195 to 188.

“It’s true there was less activity in many areas in 2015; for example, the oil and gas sector was quiet due to the falling oil price,” says Terence Tung, Mayer Brown JSM’s newly elected Asia senior partner. “But it doesn’t mean all business has gone down. There are plenty of new opportunities, such as those brought about by China’s ‘one belt, one road’ initiatives.”

Instead of increasing headcount Tung says the firm’s focus is on efficiency.

“There are plenty of new opportunities, such as those brought about by China’s ‘one belt, one road’ initiatives.”

“In today’s business environment firms can’t tolerate serious underperformance,” he says. “For us, it’s about the same workforce achieving higher productivity.”

Clifford Chance, the second-largest international firm in Hong Kong, has retained a similarly sized team, adding just one lawyer in 2015 to take its numbers to 161. The magic circle firm also grew its partnership in Hong Kong by three in 2015, to 36.

Several other of the bigger players in town including Hogan Lovells, Jones Day, Latham & Watkins and Paul Hastings have slimmed their lawyer numbers slightly.

International firms’ performance has varied widely over the past year, but they generally face a similar set of challenges such as talent retention, low vacancy rates and high rents for office space in the Central district.

Fitter for purpose

The gradual downscaling of some established firms was just one side of the complicated Hong Kong story in 2015. Conversely, some firms increased their lawyer headcount.

Ropes & Gray, for example, is one of the fastest growing firms in Hong Kong. Its number of lawyers in the office jumped 54 per cent, from 39 in 2014 to 60.

Chicago-headquartered private equity heavyweight Kirkland & Ellis has also built up its Hong Kong practice steadily in recent years. In 2015 the Hong Kong office had 64 lawyers including 29 partners, more than double its 25 lawyers in 2011, after the firm significantly expanded its Hong Kong presence by hiring eight partners from Allen & Overy, Latham and Skadden Arps Slate Meagher & Flom.

Kirkland’s Hong Kong corporate partner Nicholas Norris says 2015 was a good year across the board for the firm in Asia, and the first full year of its Hong Kong restructuring practice has been a particular success.

Deacons continues to hold its position as the city’s largest firm. With 230 lawyers, it is also ranked as the 66th largest independent firm in this year’s Asia-Pacific 150. Despite being the biggest Deacons grew again in 2015, increasing its lawyer workforce by 22 per cent, from 188 in 2014 to 230.

Sample market analysis: South Korea

Despite South Korea’s sluggish economy and the increasing presence of foreign firms in the country, the six largest firms in the jurisdiction are bullish after a strong 2015.

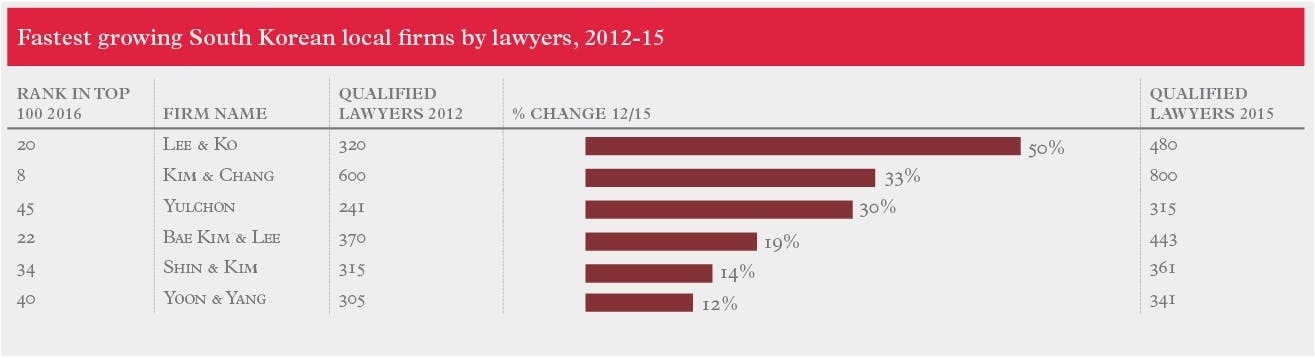

In terms of lawyer headcount, five of the country’s six biggest firms have reported growth for 2015. Kim & Chang has retained its position as the country’s most dominant firm with 800 qualified lawyers, up 5 per cent from 760 in 2014. Lee & Ko is second with 480 lawyers, up 6 per cent from last year’s 451. Bae Kim & Lee (BKL) comes third, having grown its lawyer numbers by 12 per cent, from 394 in 2014 to 443. Shin & Kim remains in fourth place with a static headcount of 361, while Yoon & Yang sees a slight increase of 5 per cent, from 350 to 341. Yulchon, the smallest of the top six players, has seen the strongest increase in headcount, 12.5 per cent, adding 35 lawyers during 2015 to push its total to 315.

No Korean firms provided revenue figures for 2015. However, a recent article published by local newspaper Maeil Business unveiled the financial standings of the top six players. According to the newspaper the six collectively turned over 1,788bn Won ($1.5bn) in 2015. Kim & Chang accounted for almost half – 49.9 per cent – of the total, with $750m. The firm’s 2015 revenue represents a 6.6 per cent increase from $703 in 2013.

In terms of revenue BKL reclaims second place by raking in $204m. However, the gap between first and second place is staggering, with Kim & Chang’s annual income more than three times that of its closest rival. In 2015 BKL returned to growth with a 22.5 per cent increase in revenue. In 2014 its figure dipped slightly, from $167m in 2013 to $166m. Lee & Ko is not far behind on $183m, having enjoyed growth over the past five years.

Yulchon jumps up the ranks to fourth when measured by annual turnover, ahead of larger rivals Shin & Kim and Yoon & Yang. The firm reported a 6 per cent increase in its 2015 revenue, up to $137m from $129m.

A busy year for locals

The strong growth of the country’s dominant legal advisers was driven by an active M&A dealmaking environment in 2015, as well as a surging number of contentious matters due to the government’s stronger and tougher enforcement actions over corruption, tax evasion and anti-competitive practices.

According to Yulchon’s founding and managing partner Yun Sai Ree, 2015 was one of the busiest years the firm has ever had. The most high-profile transaction it acted on was South Korean private equity firm MBK Partners’ $6bn acquisition of retail chain Homeplus from Tesco. It was the local adviser to MBK Partners alongside international adviser Cleary Gottlieb Steen & Hamilton. BKL and Freshfields Bruckhaus Deringer represented Tesco on the deal.

M&A boom

Yun says big-ticket M&A deals like this helped Yulchon’s corporate department achieve the strongest growth in the firm. However, he notes that most of the transactions in 2015 involved foreign investors offloading South Korea businesses, and domestic buyers. For example, another major deal the firm was involved in, Mirae Asset Financial Group’s $2bn acquisition of a stake in Daewoo Securities, falls into the latter category. The deal will create the country’s biggest brokerage firm by assets.

Apart from transactional practice Yulchon has also seen strong caseflow for contentious matters such as intellectual property (IP) and tax litigations, and antitrust investigations.

Yulchon’s larger rivals BKL and Kim & Chang also benefited from a busy year for M&A in South Korea and saw rising demand for dispute, restructuring and regulatory services.

Thomson Reuters’ South Korea M&A data shows Kim & Chang and BKL topping last year’s legal adviser league table for South Korea-related transactions by deal value. Kim & Chang advised on 121 deals valued at $56.9bn, while BKL bagged 80 with a combined value of $38bn.

BKL corporate partner Sky Young attributes the strong M&A dealflow to three key market trends: active engagement of private equity houses; surging investment from Chinese companies; and the restructuring of major Korean conglomerates such as Samsung and SK Group.

Last year BKL was involved in a number of M&A deals by Chinese acquirers, including advising Suning Group on the acquisition of technology firm Redrover and acting for Korean insurance group Tong Yang Life Insurance in its acquisition by China’s Anbang Life Insurance for $1bn. In terms of transactions arising out of corporate restructuring the firm won its fair share of deals last year, such as the merger between SK C&C and SK Holdings, that between Hana Bank and Korea Exchange Bank, and Samsung’s sell-off of four non-core businesses to Hanwha.

On the litigation front the firm had an exceedingly busy year. One of the major cases it handled saw it representing state-owned Korea Railroad (Korail) in a $8.5bn dispute between public investor Korail, Project Financing Vehicle and private investors as a result of the suspension of the Yongsan International Business District Project known as Dream Hub.

All the large firms have seen a strong uptick in antitrust investigation and litigation cases. To support growing demand from clients, they have been recruiting not only lawyers but also former government officials and economists to boost their capability in this area.

Sample profile: Top 20 international firms in Asia-Pacific

Clifford Chance

Clifford Chance has one of the largest regional footprints among global firms, and larger than all its magic circle rivals. In 2015 Clifford Chance had 601 fee-earners across nine offices in the region,

Clifford Chance has one of the largest regional footprints among global firms, and larger than all its magic circle rivals. In 2015 Clifford Chance had 601 fee-earners across nine offices in the region,

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}